You can profit $2,500 per month from just one ordinary single-family investment property.

No flipping. No house hacking. No niche business inside. No Airbnb to manage. Turnkey. No sledgehammer required. Just a regular, long-term rental…

… with a small down payment on, say, a $300,000 income property.

$2,500 might seem high.

How could one plain house really perform this well?

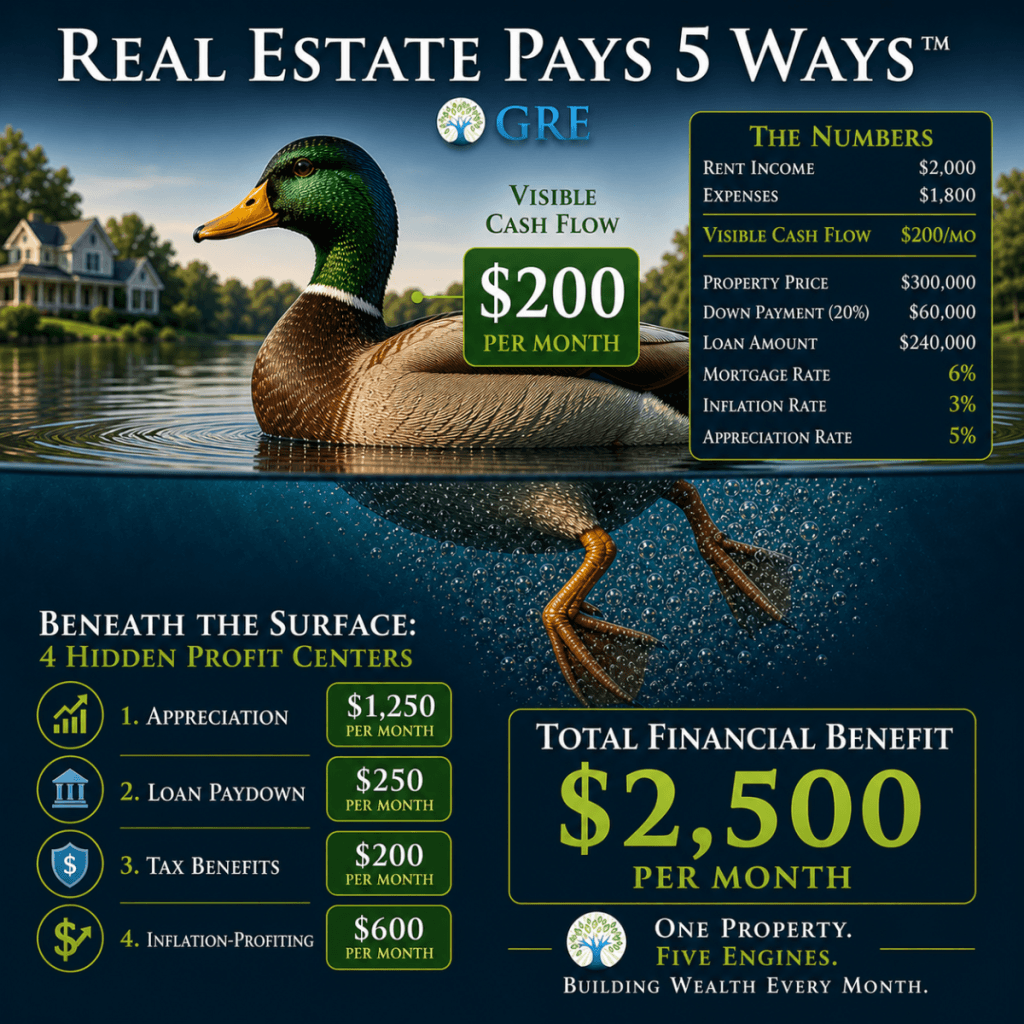

Say that it creates $200 in monthly cash flow (rent income minus expenses). This represents part of a duck that’s visible on top of the water.

The duck also kicks up less visible underwater returns of another $2,300 monthly. Here’s how.

What’s beneath the surface? Those duck legs are paddling like they’re doing CrossFit. Here’s a plausible scenario:

Appreciation of 5%

- $300,000 x 5% = $15,000 / year

- = $1,250 / month

Principal Paydown (Return on Amortization)

- Your tenant is chipping away at your loan balance

- $3,000 / year from an amort. table

- = $250 / month

Tax Benefits

- Est. depreciable value ~$240K (after land)

- $240K / 27.5 = $8,700 / year deduction

If you’re in a 25% bracket…

- Tax savings

- ~$2,200 / year

- Nearly $200 / month

Inflation-Profiting

- 3% x $240K loan = $7,200 / year

- = $600 / month

Now…

Put It All Together

- $200 Cash Flow (visible duck)

- $1,250 Appreciation

- $250 Principal Paydown

- $200 Tax Benefits

- $600 Inflation-Profiting

Your Total Financial Benefit = $2,500 / month

This is $30,000 of annual benefit to you.

That $200 per month of cash flow is only the part you can see—the duck gliding on the surface.

If it walks like a duck…

Now, of course, your exact number will be higher or lower.

Downers: A surprise insurance claim could dent it, like a tree falling onto your fence, roof leak, or plumbing backup. You’ll also have closing costs (~3% to 4% of loan amount) when you buy. The duck could get splashed.

Uppers: A refinance opportunity could increase your number. Your mortgage rate could be <6%. Many builders are buying it down to <5% for you, growing your number beyond $30K per year. The duck enjoys a tailwind.

I did some rounding for simplicity.

Essentially, this $30,000 annual benefit occurs whether you show up to work or not… and you’re probably working on it one hour per month or less.

This is simply buy-and-hold property that’s either new-build or turnkey renovated. It’s even kinda boring.

No market timing. No “next hot thing”. Nothing loud or Instagrammable.

Yet so many people miss out on all this.

Why?

Most only see the $200 visible part of the duck and think, “Why bother?”

Other investors don’t stick with it long enough to capture the benefit.

It can take a few years to really feel a wave of appreciation or inflation, or perhaps get the right refinance opportunity. These things are more apparent, like a duck that starts quacking and getting noticed.

The GRE Duck helps you understand how even a modest portfolio of five or ten ordinary properties builds lasting wealth. This is precisely how the middle class can get ahead. You could quietly out-earn your day job.